ňťĘPythonň║ôStatsmodelsńŞş´╝îŠéĘňĆ»ń╗ąńŻ┐šöĘprint(results.summary())ŠëôňŹ░ňç║ňŤ×ňŻĺš╗ôŠ×ť´╝îňŽéńŻĽňťĘńŞÇńެŔíĘŠá╝ńŞşŠëôňŹ░ňç║ňĄÜńެňŤ×ňŻĺšÜäŠĹśŔŽü´╝îń╗ąńż┐ŠŤ┤ňąŻňť░Ŕ┐ŤŔíöŔżâ´╝č

š║┐ŠÇžňŤ×ňŻĺ´╝îń╗úšáüňĆľŔç¬statsmodelsŠľçŠíú´╝Ü

nsample = 100

x = np.linspace(0, 10, 100)

X = np.column_stack((x, x**2))

beta = np.array([0.1, 10])

e = np.random.normal(size=nsample)

y = np.dot(X, beta) + e

model = sm.OLS(y, X)

results_noconstant = model.fit()

šäÂňÉÄŠłĹňÉĹŠĘíň×őŠĚ╗ňŐáńŞÇńެňŞŞÚçĆň╣Âň揊ČíŔ┐ÉŔíîňŤ×ňŻĺ´╝Ü

beta = np.array([1, 0.1, 10])

X = sm.add_constant(X)

y = np.dot(X, beta) + e

model = sm.OLS(y, X)

results_withconstant = model.fit()

ŠłĹňŞîŠťŤňťĘńŞÇň╝áŔíĘŠá╝ńŞşšťőňł░results_noconstantňĺîresults_withconstantšÜäŠĹśŔŽüŃÇéŔ┐Öň║öŔ»ąŠś»ńŞÇńŞ¬ÚŁ×ňŞŞŠťëšöĘšÜäňŐčŔ⯴╝îńŻćŠłĹňťĘstatsmodelsŠľçŠíúńŞşŠ▓튝ëŠëżňł░ń╗╗ńŻĽšŤŞňů│Ŕ»┤ŠśÄŃÇé

š╝ľŔżĹ´╝ÜŠłĹŠâ│ňł░šÜäňŤ×ňŻĺŔíĘš▒╗ń╝╝ń║Äthis´╝Ŋâ│ščąÚüôŠś»ňÉŽŠťëšÄ░ŠłÉšÜäňŐčŔ⯊ŁąŠëžŔíĄŠôŹńŻťŃÇé

šşöŠíł 0 :(ňżŚňłć´╝Ü6)

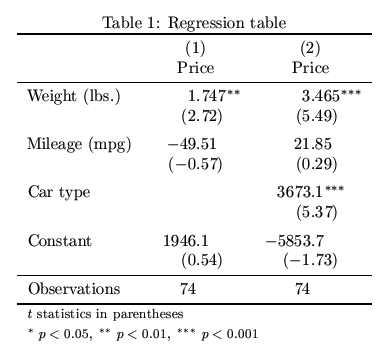

Šťësummary_col´╝çŠíúńŞşń╗Źšäš╝║ň░ĹAFAIRŃÇé

ŠłĹŔ┐śŠ▓튝뚝芺úň░ŁŔ»ĽŔ┐ç´╝îńŻćŠłĹń╗ÄńŞÇńŞ¬ÚŚ«ÚóśńŞşŠëżňł░ń║ćńŞÇńެšŤŞňů│šÜäńżőňşÉŠŁąňłáÚÖĄńŞÇń║ŤÔÇťŔ«ĘňÄîšÜäÔÇŁňĆ銼░ŃÇé

"""

mailing list, and issue https://github.com/statsmodels/statsmodels/pull/1638

"""

import pandas as pd

import numpy as np

import string

import statsmodels.formula.api as smf

from statsmodels.iolib.summary2 import summary_col

df = pd.DataFrame({'A' : list(string.ascii_uppercase)*10,

'B' : list(string.ascii_lowercase)*10,

'C' : np.random.randn(260),

'D' : np.random.normal(size=260),

'E' : np.random.random_integers(0,10,260)})

m1 = smf.ols('E ~ D',data=df).fit()

m2 = smf.ols('E ~ D + C',data=df).fit()

m3 = smf.ols('E ~ D + C + B',data=df).fit()

m4 = smf.ols('E ~ D + C + B + A',data=df).fit()

print(summary_col([m1,m2,m3,m4]))

ń╗ŹŠťëŠö╣Ŕ┐ŤšÜäńŻÖňť░ŃÇé

šşöŠíł 1 :(ňżŚňłć´╝Ü3)

ŠłĹšŤŞń┐튝ëňżłňĄÜŠľ╣Š│ĽňĆ»ń╗ąňüÜňł░Ŕ┐ÖńŞÇšé╣ŃÇéňĆľňć│ń║ÄŠéĘňĆ»ń╗ą/ňŞîŠťŤšöĘŠŁąň«×šÄ░šÜ䚍«ŠáçŃÇé

ŔÁĚšé╣ňżłňĆ»Ŕ⯊ś»šŤŞňÉîšÜä´╝Ü

statsmodels´╝ć´╝â39; linear_model´╝ć´╝â39; .fit()Ŕ┐öňŤ×RegressionResultsš▒╗´╝îňůÂńŞşsummary2()Šľ╣Š│ĽŔ┐öňŤ×ňşÉš▒╗´╝îň╣ÂňŞŽŠťëńŞÇń║ŤŠľ╣ńż┐šÜ䊾╣Š│ĽŃÇé

ňůÂńŞşńŞÇńެńżőňŽé.tablesŔ┐öňŤ×pandas.DataFrameŃÇé

ń╗ąńŞőŠś»ňŽéńŻĽńŻ┐šöĘň«â´╝Ü

import pandas as pd

results = {'Noconst':results_noconstant.summary2(),

'withcon':results_withconstant.summary2()}

df = pd.DataFrame({'Model':[], 'Param':[], 'Value':[]})

for mod in results.keys():

for col in results[mod].tables[0].columns:

if col % 2 == 0:

df = df.append(pd.DataFrame({'Model': [mod]*results[mod].tables[0][col].size,

'Param':results[mod].tables[0][col].values,

'Value':results[mod].tables[0][col+1].values}))

print df

ňô¬ńެŠöšŤŐšÄç´╝Ü

Model Param Value

0 Noconst Model: OLS

1 Noconst Dependent Variable: y

2 Noconst Date: 2016-01-29 00:33

3 Noconst No. Observations: 100

4 Noconst Df Model: 2

5 Noconst Df Residuals: 98

6 Noconst R-squared: 1.000

0 Noconst Adj. R-squared: 1.000

1 Noconst AIC: 296.0102

2 Noconst BIC: 301.2205

3 Noconst Log-Likelihood: -146.01

4 Noconst F-statistic: 9.182e+06

5 Noconst Prob (F-statistic): 4.33e-259

6 Noconst Scale: 1.1079

0 withcon Model: OLS

1 withcon Dependent Variable: y

2 withcon Date: 2016-01-29 00:33

3 withcon No. Observations: 100

4 withcon Df Model: 2

5 withcon Df Residuals: 97

6 withcon R-squared: 1.000

0 withcon Adj. R-squared: 1.000

1 withcon AIC: 297.8065

2 withcon BIC: 305.6220

3 withcon Log-Likelihood: -145.90

4 withcon F-statistic: 4.071e+06

5 withcon Prob (F-statistic): 1.55e-239

6 withcon Scale: 1.1170

ńŻ┐šöĘŠşĄňŐčŔâŻń╗ůÚÖÉń║ÄńŻ┐šöĘpandasšÜäŔâŻňŐŤ - powerful Python data analysis toolkitŃÇé

šşöŠíł 2 :(ňżŚňłć´╝Ü1)

šÄ░ňťĘŠťëńŞÇńެPython versionŠś»ń╝ŚŠëÇňĹĘščąšÜä stargazer RšĘőň║Ćňîů´╝îň«âň░▒Šś»Ŕ┐ÖŠáĚňüÜšÜäŃÇé

ňĆŽŔ»ĚňĆéÚśůń╗ąńŞőšŤŞňů│ÚŚ«Úóś´╝Ühttps://economics.stackexchange.com/q/11774/24531

šşöŠíł 3 :(ňżŚňłć´╝Ü0)

Ŕ┐ÖŠś»ńŞÇńެňĆ»Ŕ⯚Üäň«×šÄ░´╝Ü

import pandas as pd

def compare_statsmodels_ols(estimators, indice=0):

if indice in [0, 2]:

data_dict = {}

if len(estimators) > 1:

for k, est in estimators.iteritems():

data_dict[k] = est.summary2().tables[indice].iloc[:, 1::2].stack().values

index = estimators.popitem()[1].summary2().tables[indice].iloc[:, 0::2].stack().values

df = pd.DataFrame.from_dict(data_dict)

df.index = index

return df

else:

raise 'waiting for a dictionnary for estimators parameter'

else:

raise 'Not working for the coeff table'

estimators = {'m1': m1, 'm2': m2 }

compare_stats_models(estimators, 0)

m1ňĺîm2Šś»ÚóäŔúůŠĘíň×őŃÇé ŠşĄŔžúňć│Šľ╣Šíłń╗ůÚÇéšöĘń║ÄšČČńŞÇńެ´╝łindice = 0´╝ëňĺîšČČńŞëńެ´╝łindice = 2´╝ëolsŠ▒çŠÇ╗ŔíĘŃÇé

Ŕżôňç║´╝Ü

<table border="1" class="dataframe"> <thead> <tr style="text-align: right;"> <th></th> <th>m1</th> <th>m2</th> </tr> </thead> <tbody> <tr> <th>Model:</th> <td>OLS</td> <td>OLS</td> </tr> <tr> <th>Adj. R-squared:</th> <td>0.882</td> <td>0.864</td> </tr> <tr> <th>Dependent Variable:</th> <td>Mpg</td> <td>Mpg</td> </tr> <tr> <th>AIC:</th> <td>254.6367</td> <td>273.3427</td> </tr> <tr> <th>Date:</th> <td>2016-12-14 16:28</td> <td>2016-12-14 16:28</td> </tr> <tr> <th>BIC:</th> <td>389.3848</td> <td>310.7728</td> </tr> <tr> <th>No. Observations:</th> <td>312</td> <td>312</td> </tr> <tr> <th>Log-Likelihood:</th> <td>-91.318</td> <td>-126.67</td> </tr> <tr> <th>Df Model:</th> <td>35</td> <td>9</td> </tr> <tr> <th>F-statistic:</th> <td>67.12</td> <td>220.9</td> </tr> <tr> <th>Df Residuals:</th> <td>276</td> <td>302</td> </tr> <tr> <th>Prob (F-statistic):</th> <td>1.06e-114</td> <td>3.28e-127</td> </tr> <tr> <th>R-squared:</th> <td>0.895</td> <td>0.868</td> </tr> <tr> <th>Scale:</th> <td>0.11885</td> <td>0.13624</td> </tr> </tbody></table>

{kind=link}